Fill in a Valid 51A125 Kentucky Template

Kentucky PDF Forms

Fill in a Valid 51A125 Kentucky Template

The 51A125 form from Kentucky is similar to the IRS Form 1023, which is used by organizations seeking tax-exempt status under Section 501(c)(3) of the Internal Revenue Code. Both documents require detailed information about the organization’s purpose, structure, and activities. Just as the 51A125 necessitates a description of the organization’s primary functions, the IRS Form 1023 asks for a narrative that explains how the organization’s activities align with its charitable, educational, or religious mission. Both forms also require supporting documentation, such as articles of incorporation and financial statements, to substantiate the claims made within the application.

Another comparable document is the IRS Form 990, which tax-exempt organizations must file annually. Like the 51A125, Form 990 provides a comprehensive overview of an organization’s financial activities, governance, and compliance with tax regulations. Both forms aim to ensure transparency and accountability among organizations claiming tax exemptions. The 51A125 focuses on the initial application for exemption, while Form 990 serves as an ongoing report to the IRS about the organization’s financial health and adherence to its stated mission.

The Kentucky Form ST-5 is also similar to the 51A125, as it is used for sales tax exemption purposes. The ST-5 is typically employed by organizations that qualify for sales tax exemption due to their charitable or educational status. Like the 51A125, it requires the organization to provide proof of its exempt status and to detail the types of purchases for which it seeks exemption. Both forms are essential in helping organizations navigate the complexities of tax regulations while ensuring compliance with state laws.

In addition to the previously mentioned forms, the California Bill of Sale serves as a crucial document in the realm of personal property transactions, similar to how organizations must present various forms for tax exemptions. By ensuring detailed information is conveyed during the sale process, parties involved can avoid any disputes or misunderstandings down the line. Those interested in more information on crafting such documents may want to visit topformsonline.com/ for helpful resources.

The IRS Form 8868, which is an application for an extension of time to file an exempt organization return, shares similarities with the 51A125 in that both pertain to compliance with tax regulations for exempt organizations. While the 51A125 is about obtaining exemption, Form 8868 allows organizations to request additional time to file necessary documentation, ensuring that they remain compliant with IRS requirements. Both forms emphasize the importance of timely and accurate reporting to maintain tax-exempt status.

The Kentucky Form 51A131 is another document related to sales tax exemptions, specifically for nonprofit organizations. This form is used to claim exemption from sales tax on purchases made by qualifying organizations, similar to the purpose of the 51A125. Both forms require the organization to provide verification of its exempt status and detail the nature of its operations. They serve to facilitate the tax-exempt purchasing process for organizations that provide essential services to the community.

The IRS Form 990-EZ is a simplified version of Form 990 and is applicable to smaller tax-exempt organizations. Like the 51A125, it requires financial information and a description of the organization’s activities. Both forms aim to ensure that organizations maintain transparency and adhere to the rules governing tax-exempt status. The 990-EZ is designed for organizations with less complex financial situations, while the 51A125 focuses on the initial application process for tax exemption.

The Kentucky Form 51A129 is relevant as it pertains to the exemption of sales tax for certain government entities. Similar to the 51A125, this form requires entities to provide evidence of their status and the nature of their operations. Both forms facilitate the exemption process for organizations that serve public interests, ensuring that they can operate without the burden of sales tax on necessary purchases.

The IRS Form 1024 is used by organizations applying for recognition of exemption under various sections of the Internal Revenue Code, including 501(c)(4) and 501(c)(6). While the 51A125 specifically targets charitable, educational, and religious organizations, Form 1024 covers a broader range of exempt purposes. Both forms require detailed information about the organization’s structure and activities, highlighting the importance of compliance in maintaining tax-exempt status.

Finally, the Kentucky Form 51A125A is used for applications by organizations that are already registered as tax-exempt but need to apply for additional exemptions or changes. This form mirrors the 51A125 in that it requires similar documentation and information about the organization’s purpose. Both forms are crucial in ensuring that organizations can navigate the complexities of tax exemptions and maintain compliance with state regulations.

When filling out the 51A125 Kentucky form, it’s crucial to follow specific guidelines to ensure a smooth application process. Here are some important dos and don'ts:

Filling out the 51A125 Kentucky form requires attention to detail and adherence to specific guidelines. Below are key takeaways to consider when using this form.

Kentucky Ui 1 - Part VI outlines the process for businesses acquiring existing operations and requires details from both parties.

Form 740 - Estimated quarterly withholding amounts must be reported if applicable.

To ensure a successful vehicle sale, it is essential to consider essential resources such as the Templates and Guide, which provide valuable insights into the California Vehicle Purchase Agreement form that outlines the key terms and conditions necessary for a clear transaction.

Kentucky Workers Compensation Insurance - Each claimant needs to sign the form, attesting to the truthfulness of their statements.

What is the purpose of the 51A125 Kentucky form?

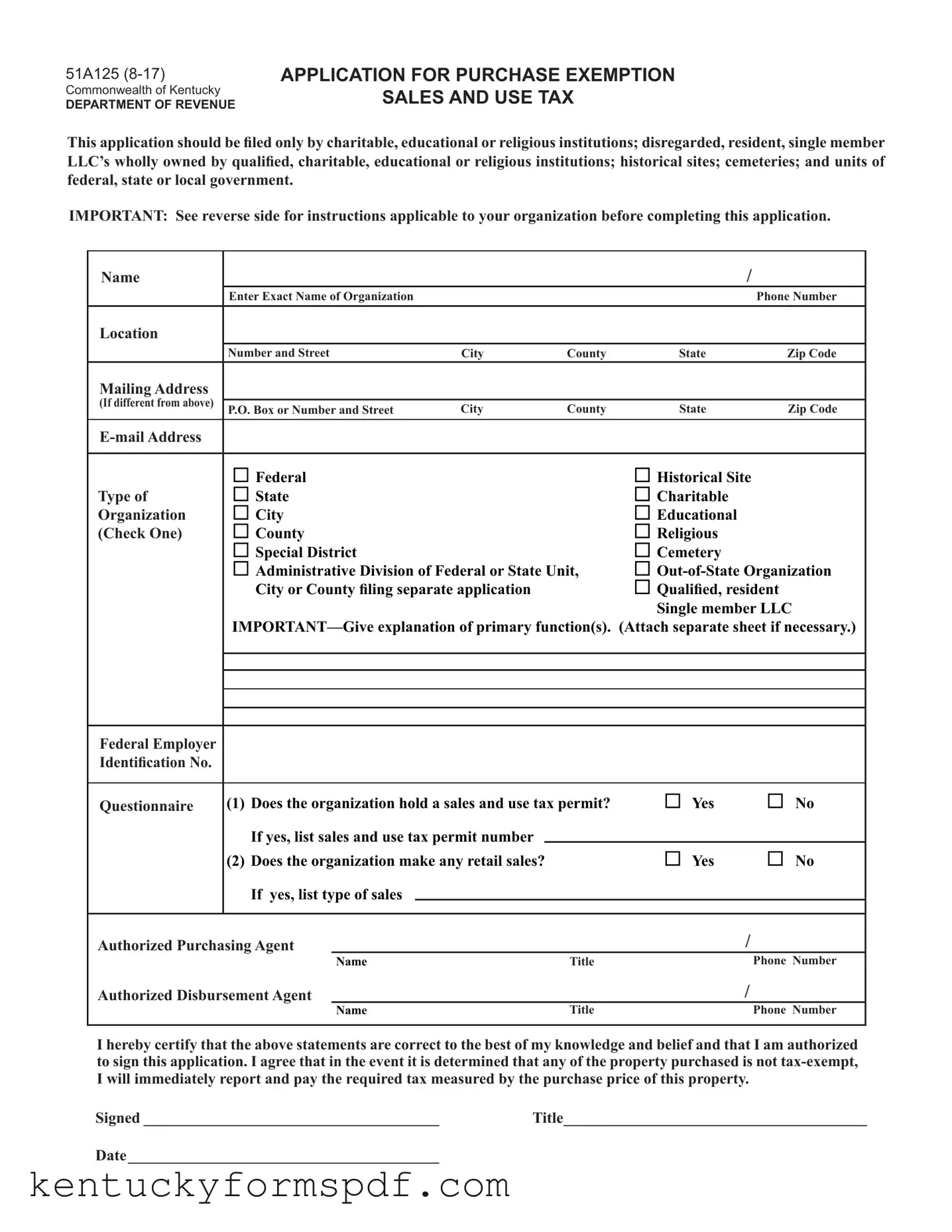

The 51A125 form is an application for purchase exemption from sales and use tax in Kentucky. It is specifically designed for charitable, educational, or religious institutions, as well as certain government units and historical sites. By completing this form, eligible organizations can obtain tax-exempt status for their purchases, allowing them to buy tangible personal property and services without paying sales tax, provided the items are used within their exempt functions.

Who is eligible to file the 51A125 form?

Eligibility to file the 51A125 form includes a variety of organizations. Charitable, educational, and religious institutions can apply, as can historical sites, cemeteries, and local, state, or federal government units. Additionally, disregarded, resident single-member LLCs that are wholly owned by qualified organizations are also eligible. Each applicant must meet specific criteria and provide documentation to support their status, such as proof of tax-exempt status from the IRS or confirmation of listing in the National Register for historical sites.

What documents must be submitted with the 51A125 form?

When submitting the 51A125 form, certain documents must accompany the application to ensure eligibility. Charitable, educational, and religious institutions need to attach a copy of their Articles of Incorporation, a detailed schedule of receipts and disbursements, and a letter from the IRS confirming their tax-exempt status under Section 501(C)(3). Historical sites must include a letter from the Kentucky Heritage Commission. For cemeteries, a copy of their Articles of Incorporation and a property tax exemption ruling are required. Government units must provide registration documents as specified by Kentucky law.

What happens if the application is approved?

If the application for the 51A125 form is approved, the organization will receive a letter of authorization that includes an exemption number. This allows the organization to make tax-exempt purchases of tangible personal property and services related to their exempt functions. However, it is important to note that any purchases not used for exempt purposes will still be subject to sales tax. Additionally, if the organization engages in taxable sales and is not classified as an educational or charitable institution, it must obtain a sales and use tax permit.