Fill in a Valid Kentucky Qcc1 Template

Kentucky PDF Forms

Fill in a Valid Kentucky Qcc1 Template

The Kentucky QCC1 form is similar to the IRS Form 941, which is the Employer's Quarterly Federal Tax Return. Both documents are designed to report income tax withheld from employees' wages and the employer's share of Social Security and Medicare taxes. Employers must file these forms quarterly, ensuring that they accurately reflect the amounts withheld during the reporting period. The QCC1 focuses on local withholding, while Form 941 addresses federal obligations, making them both essential for compliance with tax regulations.

Another document comparable to the Kentucky QCC1 is the State of Kentucky Form K-1, which is used for reporting income tax withheld on behalf of employees. Like the QCC1, the K-1 form requires employers to provide detailed information about employee earnings and the corresponding tax withheld. Both forms ensure that employers fulfill their tax responsibilities, though the K-1 is specifically for state income tax, while the QCC1 incorporates local tax requirements.

The W-2 form is another important document that shares similarities with the QCC1. While the QCC1 is a quarterly report, the W-2 is an annual summary of an employee's earnings and tax withholdings. Employers use the W-2 to report total earnings and taxes withheld for each employee over the entire year. Both forms are crucial for ensuring accurate reporting and compliance with tax obligations, providing a clear record of earnings and withholdings.

Understanding the intricacies of tax reporting forms is essential for compliance and accuracy in payroll management. For instance, the Kentucky QCC1 form, which resembles the IRS Form 941, serves a critical role in employers’ reporting obligations. As part of maintaining confidentiality, especially when dealing with sensitive employee data, utilizing a https://floridaformspdf.com/printable-non-disclosure-agreement-form/ can ensure that businesses protect proprietary information when handling taxes and payroll documentation.

Form 1099-MISC also bears resemblance to the Kentucky QCC1, particularly in the context of reporting income. While the QCC1 is focused on employee wages, the 1099-MISC is used to report payments made to independent contractors and other non-employee compensation. Both forms require accurate reporting of earnings and tax information, but they serve different categories of workers, highlighting the diverse nature of income reporting requirements.

The Local Business Tax Return is another document that aligns with the QCC1. Local governments often require businesses to report their earnings and pay taxes based on their income. Similar to the QCC1, this return ensures that local tax obligations are met, and it typically requires detailed information about the business's earnings and any applicable deductions. Both forms emphasize the importance of local compliance in tax matters.

Form 940, the Employer's Annual Federal Unemployment (FUTA) Tax Return, is also comparable to the QCC1. While the QCC1 focuses on income tax withholdings, Form 940 is specifically for reporting unemployment taxes owed by employers. Both forms are essential for maintaining compliance with tax regulations, but they address different aspects of employment-related taxes. Employers must file both forms to ensure they meet their federal and local tax obligations.

The Kentucky Employer's Wage Report is similar to the QCC1 in that it also requires reporting on employee wages and tax withholdings. This report is typically filed with the state and ensures that employers are meeting their obligations for unemployment insurance and other state taxes. Both documents require accurate reporting of employee earnings and are crucial for compliance with state tax laws.

The Federal Information Form 945 is another document that shares similarities with the Kentucky QCC1. This form is used to report income tax withheld from non-payroll payments, such as pensions and annuities. While the QCC1 focuses on payroll withholding for employees, both forms require accurate reporting of tax withholdings and compliance with federal regulations.

Finally, the Federal Form 1065, used for partnerships, bears some resemblance to the QCC1. Both documents require reporting of earnings and tax obligations, though the 1065 is specifically for partnerships and includes information about each partner's share of income. While the contexts differ, both forms emphasize the importance of transparency and accuracy in reporting financial information to tax authorities.

When filling out the Kentucky QCC1 form, it's essential to follow specific guidelines to ensure accuracy and compliance. Here’s a list of things to do and avoid:

When filling out the Kentucky QCC1 form, there are several important points to keep in mind to ensure accuracy and compliance.

By keeping these key takeaways in mind, you can navigate the QCC1 form process more confidently and effectively.

Map 350 - It plays a critical role in enhancing the quality of life for Medicaid waiver participants.

In addition to understanding the core aspects of the California Vehicle Purchase Agreement, it is beneficial to refer to resources that can provide further insights on the process, such as Templates and Guide, which can assist in navigating the necessary documentation for a seamless vehicle transaction.

Kentucky Ui 1 - Understanding each part of the UI-1 helps ensure no section is overlooked, promoting complete transparency.

What is the Kentucky QCC1 form used for?

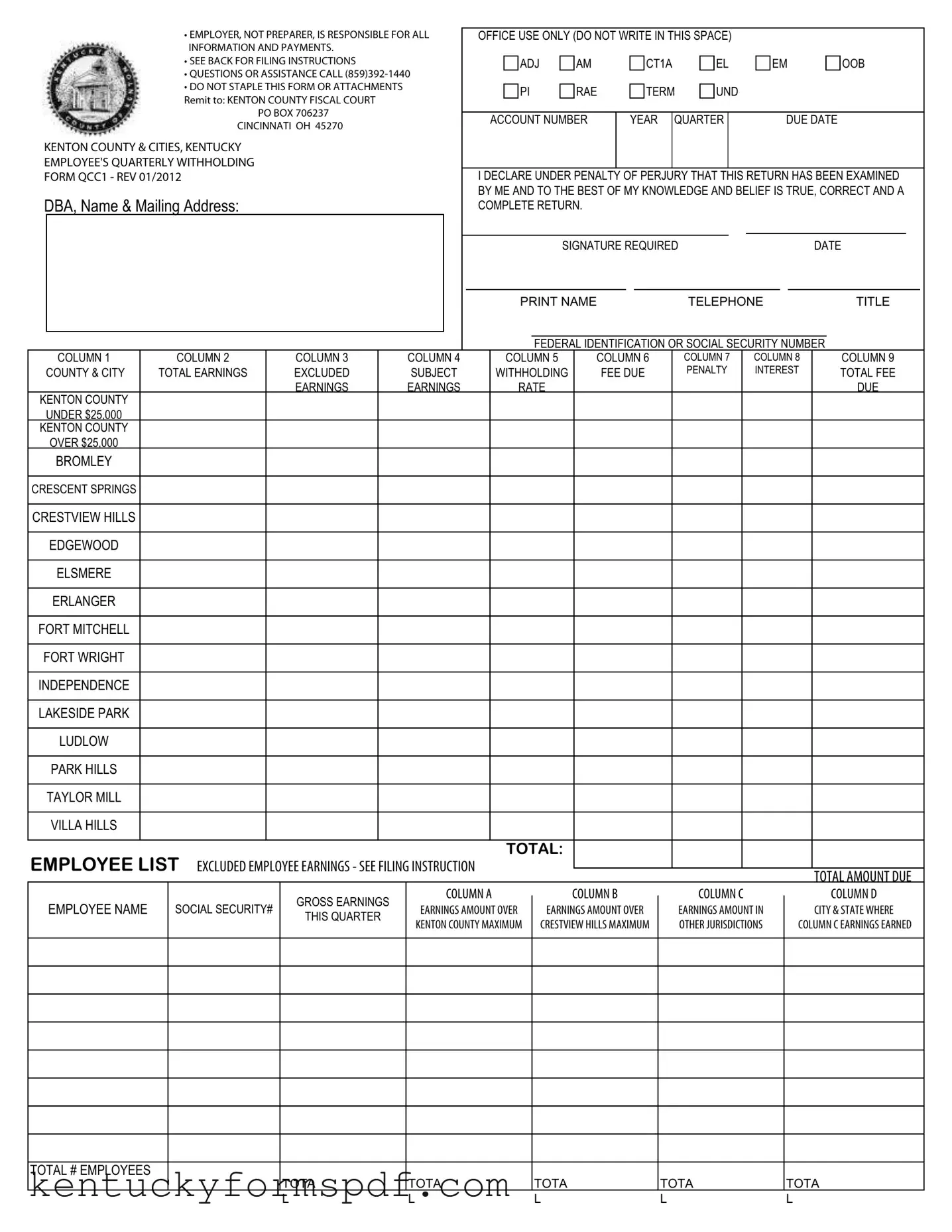

The Kentucky QCC1 form is primarily used by employers to report employee earnings and withholdings for Kenton County and its cities. This quarterly withholding form captures important information regarding total earnings, excluded earnings, and the applicable withholding fees. It ensures that employers comply with local tax regulations and accurately report their employees' earnings to the Kenton County Fiscal Court.

Who is responsible for completing the QCC1 form?

The employer holds the responsibility for completing and submitting the QCC1 form. It is crucial that the employer ensures the accuracy of the information provided, as they are liable for any errors or omissions. The preparer of the form, if different from the employer, does not assume responsibility for the accuracy of the information or payments. Therefore, employers should carefully review the form before submission to avoid penalties.

What information is required on the QCC1 form?

When filling out the QCC1 form, employers must provide several key pieces of information. This includes the employer's name and mailing address, the federal identification number or social security number, total earnings for the quarter, and the applicable withholding fees. Additionally, employers must report any excluded earnings and provide a detailed list of employees, including their names, social security numbers, and earnings amounts. The form also requires a declaration under penalty of perjury, affirming the accuracy of the information submitted.

What should I do if I have questions about the QCC1 form?

If you have questions or need assistance regarding the QCC1 form, you can reach out to the Kenton County Fiscal Court at (859) 392-1440. They can provide guidance on filling out the form, understanding the filing instructions, and addressing any specific concerns you may have about your submission. It’s always better to seek clarification than to risk errors in your filing.

What happens if the QCC1 form is filed incorrectly or late?

Filing the QCC1 form incorrectly or after the due date can result in penalties and interest charges. The form outlines the potential fees due based on the earnings reported, and any inaccuracies may lead to additional penalties. Employers should strive to file the form on time and ensure all information is correct to avoid these financial repercussions. If you find that you have made an error after submission, it is advisable to contact the Kenton County Fiscal Court immediately for guidance on correcting the mistake.