Valid Promissory Note Template for Kentucky State

Kentucky PDF Forms

Valid Promissory Note Template for Kentucky State

A promissory note is a financial instrument that reflects a promise to pay a specific amount of money to a designated person or entity at a defined future date. It shares similarities with a loan agreement, which is a more detailed document outlining the terms and conditions of a loan. While a promissory note typically includes the amount borrowed, interest rate, and repayment schedule, a loan agreement goes further by specifying the rights and obligations of both the lender and borrower, including any collateral involved and the consequences of default. Both documents serve to formalize the borrowing process and provide legal recourse in case of non-payment.

A mortgage is another document that bears resemblance to a promissory note. In a mortgage agreement, the borrower pledges real property as collateral for the loan. The promissory note accompanies the mortgage, detailing the borrower's promise to repay the loan amount. While the promissory note focuses on the borrower's obligation to pay, the mortgage secures that obligation by granting the lender a claim on the property. In essence, both documents work together to protect the lender's interests while providing the borrower with access to funds.

A personal guarantee is similar in that it provides assurance to a lender regarding the repayment of a debt. In this document, an individual agrees to be personally responsible for the debt if the primary borrower defaults. Like a promissory note, it establishes a clear obligation to pay. However, a personal guarantee adds an additional layer of security for the lender, as it allows them to pursue the guarantor’s personal assets in the event of default. Both instruments emphasize the importance of trust and accountability in financial transactions.

A loan application can also be compared to a promissory note, though it serves a different purpose. The loan application is the initial document submitted by a borrower seeking funds, detailing their financial situation and reasons for borrowing. While a promissory note is created after the loan is approved and outlines the terms of repayment, the loan application is the starting point for the lending process. Both documents are crucial in establishing the relationship between borrower and lender, with the loan application laying the groundwork for the terms that will later be formalized in the promissory note.

To enhance your application process for a position at Chick-fil-A, utilizing resources such as Templates and Guide can provide you with structured assistance, ensuring that you complete the application form effectively and impressively.

An installment agreement is another document that shares characteristics with a promissory note. This agreement outlines a borrower’s commitment to repay a debt in regular, scheduled payments over time. Like a promissory note, it includes details about the total amount owed, interest rates, and payment frequency. However, an installment agreement may also include additional terms, such as penalties for late payments or provisions for early repayment. Both documents aim to clarify the repayment process and protect the interests of the lender while ensuring the borrower understands their obligations.

A security agreement can be likened to a promissory note in that it provides a lender with rights to specific collateral in the event of default. In a security agreement, the borrower grants the lender a security interest in certain assets, which can be seized if the borrower fails to repay the loan. The promissory note, on the other hand, focuses on the borrower's promise to repay the loan amount. Both documents work in tandem to create a framework for securing the lender’s investment while providing the borrower with the necessary funds.

Finally, a lease agreement has similarities to a promissory note in that it establishes a payment obligation over a specified period. In a lease agreement, a tenant agrees to pay rent to a landlord in exchange for the use of property. Like a promissory note, it outlines the amount due, payment schedule, and consequences of non-payment. While the contexts differ—one being for borrowing money and the other for renting property—the underlying principle of creating a binding obligation to pay is common to both documents.

When filling out the Kentucky Promissory Note form, attention to detail is crucial. Here are seven important do's and don'ts to keep in mind:

Following these guidelines will help ensure that the Promissory Note is valid and enforceable. Properly completing the form can prevent misunderstandings in the future.

When filling out and using the Kentucky Promissory Note form, it is important to keep several key points in mind to ensure clarity and legal validity.

Divorce Templates - The agreement provides a structure for spousal support or alimony obligations.

The process of establishing a corporation in Ohio necessitates a well-prepared set of documents. For instance, utilizing a proper form for your Articles of Incorporation can be paramount, as it allows you to navigate state requirements efficiently. For more guidance, you can refer to this informative resource on optimal Articles of Incorporation procedures.

Power of Attorney Kentucky - This document allows for broad or limited authority depending on your needs.

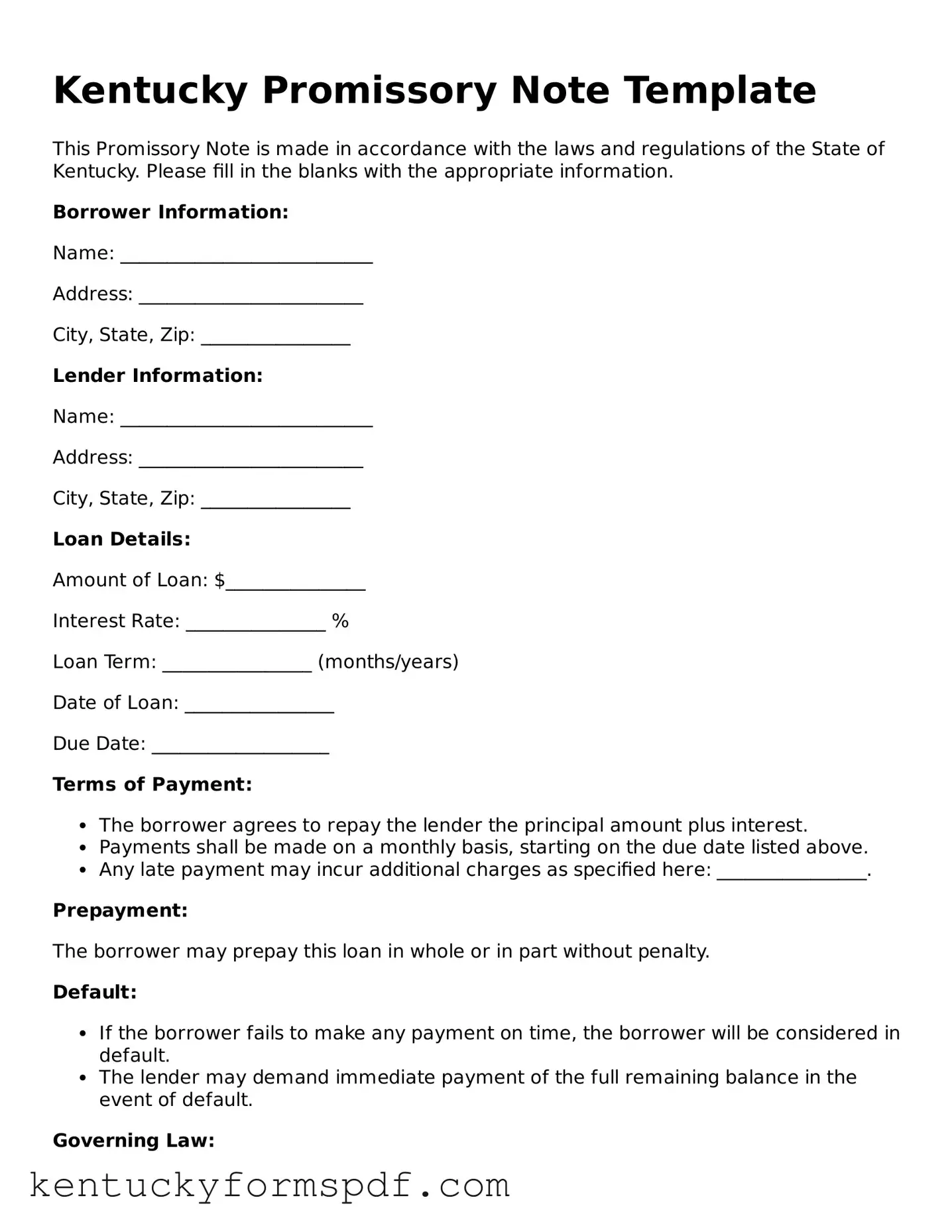

What is a Kentucky Promissory Note?

A Kentucky Promissory Note is a legal document that outlines a borrower's promise to repay a specified amount of money to a lender under agreed-upon terms. This document serves as a written record of the debt and includes details such as the loan amount, interest rate, repayment schedule, and any penalties for late payments. It is essential for both parties to have a clear understanding of their obligations.

Who needs a Promissory Note?

Anyone involved in a loan transaction in Kentucky should consider using a Promissory Note. This includes individuals lending money to friends or family, businesses extending credit to customers, or any financial institution providing loans. Having a formal agreement helps protect both the lender's and borrower's rights, ensuring that expectations are clear and legally enforceable.

What are the key components of a Kentucky Promissory Note?

Key components of a Kentucky Promissory Note include the names and addresses of both the borrower and lender, the principal amount borrowed, the interest rate, the repayment schedule, and any collateral involved. Additionally, it should specify the consequences of default, such as late fees or legal action. A well-drafted note will also include the date of the agreement and any applicable state laws.

Is it necessary to have the Promissory Note notarized?

While notarization is not strictly required for a Promissory Note to be valid in Kentucky, it is highly recommended. Notarizing the document adds an extra layer of authenticity and can help prevent disputes over the validity of the agreement. It serves as proof that both parties willingly entered into the agreement, which can be crucial in legal situations.

Can a Promissory Note be modified after it is signed?

Yes, a Promissory Note can be modified after it is signed, but both parties must agree to the changes. It is advisable to document any modifications in writing and have both parties sign the amended agreement. This ensures that all parties are aware of the new terms and helps prevent misunderstandings in the future.

What happens if the borrower defaults on the Promissory Note?

If the borrower defaults on the Promissory Note, the lender has several options. They may pursue legal action to recover the owed amount, which could involve filing a lawsuit. The lender may also seek to collect through other means, such as wage garnishment or placing a lien on the borrower's property. It is crucial for both parties to understand their rights and responsibilities in the event of default.